You are currently viewing this website using the Internet Explorer (IE) web browser. This website has limited functionality in IE, and you won’t be able to download research documents. For an optimal experience, please access this website using any other supported web browser.

Underlying fund performance, asset allocation, and cash flows of more than 100 large defined contribution plans representing approximately $400 billion in assets are tracked in the Callan DC Index.

Index Starts 2025 with a Loss

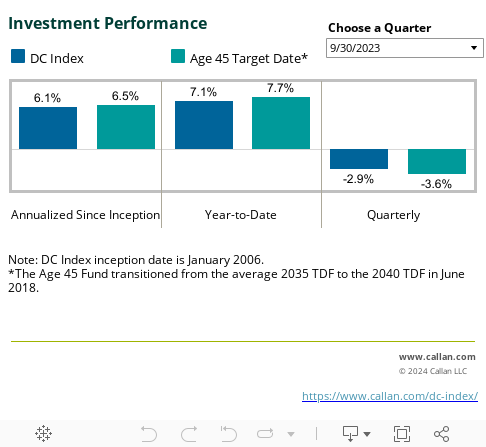

The Callan DC Index™ lost 1.5% in 1Q25, which brought the Index’s trailing one-year return to 5.6%. The Age 45 Target Date Fund (analogous to the 2045 vintage) had a higher quarterly return (-0.4%) and a higher trailing one-year return (+6.1%). Over longer time horizons, the Age 45 TDF’s higher relative equity allocation has contributed to a higher annualized since-inception* return (7.3% vs. 6.9%).

*The Index was created in 2006.

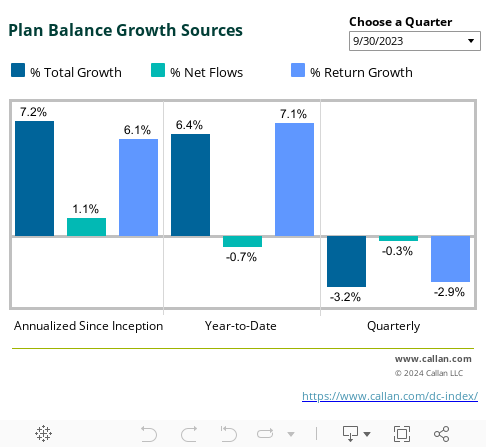

Balances Fall Due to Investment Losses

Balances within the DC Index fell by 1.9% after a 0.8% decrease in the previous quarter. Investment losses (-1.5%) were the primary cause as net flows (-0.4%) fell less. The net flows figure will continue to provide a critical measure of how effectively plans retain the balances of retiring participants, who often own an outsized share of total plan assets.

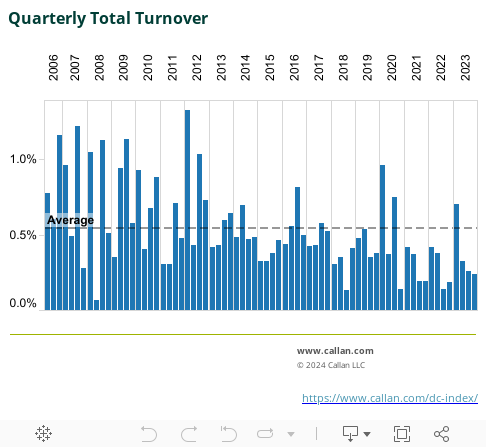

Turnovers Rise for Second Straight Quarter

Turnover (i.e., net transfer activity levels within DC plans) increased to 0.27% from the previous quarter’s 0.11%. The Index’s historical average (+0.52%) remained steady.

U.S. Equity Falls Sharply for Third Straight Quarter

Automatic features and their appeal to “do-it-for-me” investors typically result in target date funds (TDFs) receiving the largest net inflows in the DC Index. Target date funds earned 44.9% of quarterly net flows. Money market and U.S. fixed income funds also received a large portion of inflows, (23.5%) and (20.4%) respectively.

Notably, within equities, investors withdrew assets from U.S. large cap equity (-46.5%) and U.S. small/mid-cap equity (-20.3%), similar to the large outflows of the previous quarter.

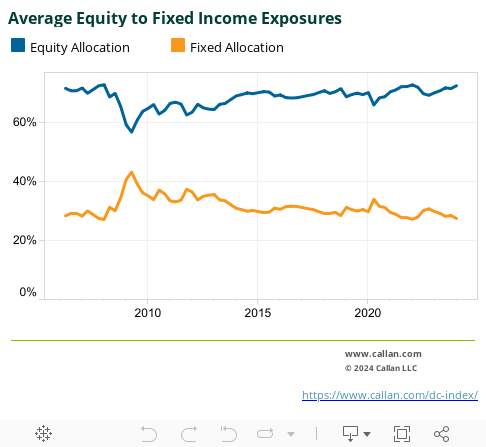

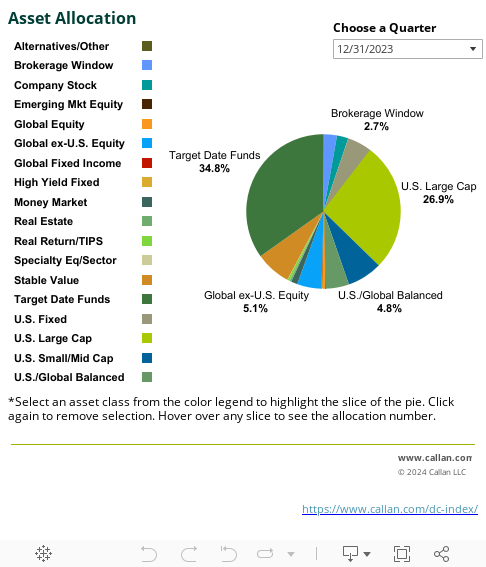

Exposure Falls

The Index’s overall allocation to equity (73.8%) fell slightly from the previous quarter’s level (74.4%). The current equity allocation continues to sit above the Index’s historical average (68.9%).

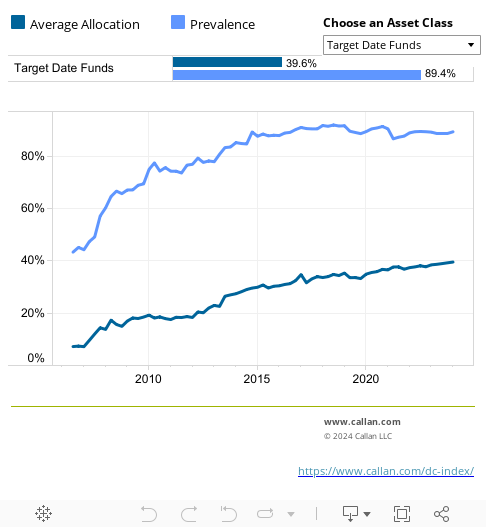

Target Date Funds Gain

Target date funds (36.5%), global ex-U.S. equity (5.0%), and U.S. fixed income (5.2%) were among the asset classes with the largest percentage increases in allocation. U.S. large cap equity (28%) and U.S. small/mid cap equity (6.5%) had the largest decreases in allocation from the previous quarter.

Brokerage Windows Fall

In the prevalence of funds table, the green bars indicate the prevalence of asset classes within DC plans, while the blue bars show the average allocation to particular asset classes when offered as an option.

The prevalence of brokerage windows (43.4%) fell by 0.8 percentage points. Other notable movements included a 0.6 percentage point increase in the prevalence of real return/TIPS fund offerings (38.2%).

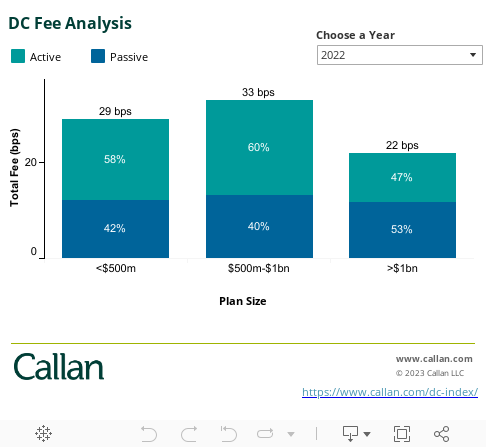

The DC Fee Analysis chart shows the average total investment management fee by plan size, as well as the average share of plan assets allocated to active and passive options. Fees for each fund (including mutual funds, collective trusts, and separate accounts) within a plan are asset-weighted to determine the average total fee. This exhibit will be updated annually with the release of third quarter DC Index results, and this updated data should be available shortly.

Using 3Q23 data, for plans with assets less than $500 million in assets, the average asset-weighted fee decreased by 3 basis points from 3Q22. Plans with assets between $500 million and $1 billion saw the largest fee decrease of 9 bps, while the fee for plans with more than $1 billion in assets had a decrease of 4 bps. Fee decreases were largely driven by a combination of increased use of passive mandates as well as lower breakpoints and new lower fee vehicles and share classes for actively managed options.

For Investment Managers & Advisers

You are now leaving Callan LLC’s website and going to Callan Family Office’s website. Callan Family Office is not affiliated with Callan LLC. Callan LLC has licensed the Callan® trademark to Callan Family Office for use in providing investment advisory services to ultra-high net worth clients, family foundations, and endowments. Callan Family Office and Callan LLC are independent, unaffiliated investment advisory firms separately registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

Callan LLC is not responsible for the services and content on Callan Family Office’s website. Inclusion of this link does not constitute or imply an endorsement, sponsorship, or recommendation by Callan LLC of their website, or its contents, and Callan LLC is not responsible or liable for your use of it. When visiting their website, you are subject to Callan Family Office’s terms of use and privacy policies.