You are currently viewing this website using the Internet Explorer (IE) web browser. This website has limited functionality in IE, and you won’t be able to download research documents. For an optimal experience, please access this website using any other supported web browser.

Listen to This Blog Post

June 30 is the most common fiscal year end for public defined benefit (DB) plans, making second quarter performance data an important measurement period. In the fiscal year ended June 30, 2025, the median public pension plan gained 11.3%, well in excess of the median assumed rate of return of 7.00%.

This marks the third consecutive fiscal year where the median public DB plan’s return was well in excess of the assumed rate of return (2023: 8.9%; 2024: 10.6%). This bodes well for an improvement in funded status across public plans. Many utilize an actuarial smoothing period of five years, and over the last five years, the median public pension had an annualized return of 9.3%.

All of the major asset classes ended the last 12 months with gains, led by global ex-U.S. equities (MSCI ACWI ex-USA: 17.7%), U.S. equities (Russell 3000: 15.3%), and core fixed income (Bloomberg Aggregate: 6.1%). Real estate (NCREIF Property Index: 4.2%) bounced back after being a notable laggard the previous two fiscal years. Dispersions in results by plan size once again were dictated by relative allocations to private markets assets. Small plans’ more liquid portfolios benefited as public equities generated double-digit returns, while private markets portfolios continue to play catch-up with their marks. Private credit, where many large institutional investors are increasing allocations, underperformed their public market equivalents (high yield and bank loans).

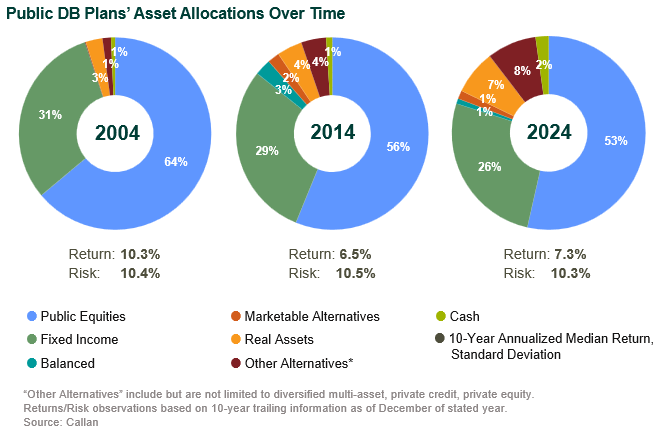

Over the 10-year timeframe, larger plans have outperformed their smaller peers. The illiquidity premium has benefited results, most particularly when comparing plain vanilla fixed income (Bloomberg Aggregate: 1.8%) versus more complex diversifiers (Cambridge Senior Debt: 7.1%, NCREIF Property Index: 5.2%) where bigger plans have larger exposures.

Larger plans generally have higher allocations to private assets due to the advantages their scale provides them. While many plans are revisiting their asset-allocation targets given the secular change in fixed income return expectations, there is still a significant funding gap that will require public plans to seek higher returns via more complex and illiquid asset classes.

Despite the short-term return dispersions, plans should continue to make strategic decisions based on their long-term objectives, rather than reacting to what has worked in the markets lately. While market-timing decisions may capture cocktail hour conversations and flashy headlines, the long-term approach has worked out over time as the median public plan’s 10-year return has consistently exceeded the median return hurdle (7.00%). As always, Callan recommends public plans should focus on their ability to achieve their long-term expected return on assets (EROA) target rather than fixating on short-term volatility.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.

For Investment Managers & Advisers

You are now leaving Callan LLC’s website and going to Callan Family Office’s website. Callan Family Office is not affiliated with Callan LLC. Callan LLC has licensed the Callan® trademark to Callan Family Office for use in providing investment advisory services to ultra-high net worth clients, family foundations, and endowments. Callan Family Office and Callan LLC are independent, unaffiliated investment advisory firms separately registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

Callan LLC is not responsible for the services and content on Callan Family Office’s website. Inclusion of this link does not constitute or imply an endorsement, sponsorship, or recommendation by Callan LLC of their website, or its contents, and Callan LLC is not responsible or liable for your use of it. When visiting their website, you are subject to Callan Family Office’s terms of use and privacy policies.